.webp)

.webp)

NRI Income Tax Filling in India - Simple, Complaint & Expert Led

Earning income in India while living abroad? Whether you're an NRI, OCI, or foreign national, you may be required to file a tax return under Indian law.

At AAGC, we offer end-to-end assistance to help you stay compliant, claim deductions, and file on time — with zero hassle.

- Personalized advisory

- Expert-assisted and prepared ITRs

- Secure Data Sharing

Trusted by global Indians across 5+ countries. Speak to an Expert

AAGC Advantage

NRI Tax Expertise

Simplify residential status, DTAA benefits, and global income reporting

Secure & Seamless Process

Upload, Track your ITR status, and Communicate

Timely Reminders & Guidance

Never miss a deadline or opportunity.

Trusted Across Borders

We’ve helped NRIs and foreign nationals in 5+ countries

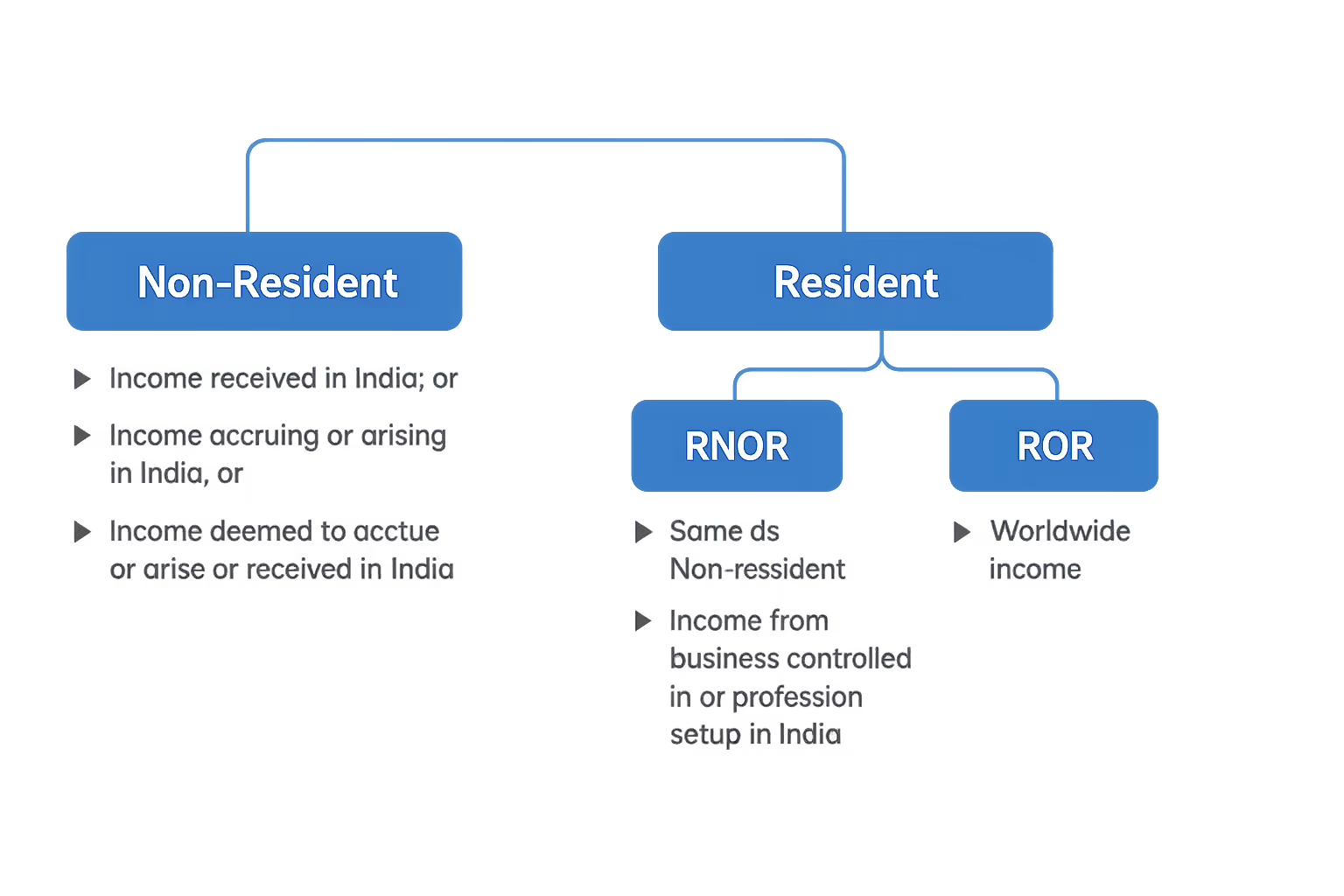

Benefit's of RNOR status for NRI's

Any person other than a resident Indian citizen is required to file income tax returns in India only on income that arises or accrues in India. The provisions of the Act can be advantageous for NRIs as they are not liable to pay income tax on the following income:

- Interest on FCNR deposits and NRE deposits if you convert that to RFC (Resident Foreign Currency Account)

- Withdrawal from offshore retirement accounts

- Rent received abroad

- Capital Gains made abroad

- Interest/Dividend received on Investments/Securities abroad

Determining NRI Status

Individuals

HUF/FIRM/AOP

Company

Deemed to be Not Ordinarily resident

An individual, being a citizen of India, having total income, other than the income from foreign sources, exceeding fifteen lakh rupees during the previous year shall be deemed to be resident in India in that previous year, if he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature.

However, as per the clarification from CBDT via press release dated 2nd February 2020 to clarify that in case of an Indian citizen who becomes deemed resident of India under this proposed provision, income earned outside India by him shall not be taxed in India unless it is derived from an Indian business or profession.

The condition for deemed residential status applies only if the total income (other than foreign sources) exceeds Rs 15 lakh and nil tax liability in other countries or territories by reason of his domicile or residence or any other criteria of similar nature.